Easy Ways to Meet Credit Card Spending Requirements Reddit

There's nothing like staring at a massive signup bonus and knowing it could be yours soon. The catch? You must spend a certain amount of money to claim it.

Some cards are tough to crack, like the Chase Sapphire Preferred® Card (you have to spend $4,000 in the first 3 months). Others offer an easier path, like the Bank of America® Travel Rewards Credit Card (you only have to spend $1,000).

Whatever the spending requirement, you'll need reach it within a specified amount of time. Otherwise, your signup bonus is gone forever.

You don't want to spend money unnecessarily just to hit the minimum spending requirements. That might erase the value of your rewards altogether. Instead, deploy your card intelligently and spend mostly on the must-haves. That way, you'll breeze by your spending requirement without shelling out extra dough.

Ready to hit that big payday? Here are 25 super-effective hacks to hit your minimum spending requirement.

You'll find that you can use your card to buy things you'd spend money on regardless. As much as you can, make those purchases with your new card.

1. Use your card all the time.

Now that you have a new card, start using it for everything. Whatever you're buying — your morning latte, movie tickets or your next book for nighttime reading — charge it to your credit card. Of course, use your card for everyday purchases like gas and groceries.

You may even get bonus points or miles for certain types of spending. For example, the PenFed Platinum Rewards Visa Signature® Card gives you an eye-popping 5x points on gas purchases at the pump. That's a sweet bonus as you're working toward your minimum spending requirement.

2. Buy gift cards for your regular shopping.

Feel like you're constantly making trips to a certain store? Consider using your credit card to buy gift cards for that location. You'll get closer to your minimum spending requirement, and you can use the gift cards for purchases you'd make anyway.

For example, if you spend $100 a week at Target, you'll spend over $1,000 within three months. You can use your credit card to buy a $1,000 Target gift card, then use the gift card for your shopping.

If you're worried about carrying a gift card with a large amount of money on it, buy multiple gift cards with smaller dollar amounts. You may even be able to send your gift card to your email address or mobile phone.

Use this strategy at other locations you frequent, such as supermarkets and gas stations. A big plus: You don't have to pay convenience fees for these gift cards, unlike with a Visa or American Express gift card.

How to avoid inadvertent cash advances

Some card providers classify gift card purchases as cash advances. You want to avoid cash advances as much as you can, because they're typically very expensive.

To get around this, ask your credit card provider to set your cash advance limit to $0. Once you do this, any transaction coded as a cash advance will be declined.

3. Pay your bills.

Many utility, car insurance and health insurance companies allow credit card payments. And it's virtually certain that you can use a card for your cable and phone bills. If you've been paying through your bank account, see if you can use your credit card instead.

4. Prepay your bills.

Most people don't know this, but you can actually prepay some of your bills. Confirm whether your service providers allow prepayments. If they do, they probably limit how much you can prepay (though that limit will likely be high).

If you're lucky, you may even get rewarded for paying early. Some providers — especially health insurance and car insurance companies — offer discounts if you buy coverage a few months at a time.

5. Use bill pay services.

You often can't pay your mortgage, car loan or rent with a credit card. But other services can pay bills on your behalf, accepting payment via credit card.

TIO (formerly ChargeSmart) and Plastiq are two bill pay services you can try. For rent, look into RadPad, RentMoola and RentShare.

To use a credit card, you'll typically have to pay a service fee of 2% or 3%. That said, this method could help you rack up spending quickly.

After you load funds with a credit card, RadPad sends a check to your landlord.

One unchanging fact of life is paying taxes to Uncle Sam. So why not time your credit card applications to coincide with tax season? That way, you can knock out your tax bill and quickly reach your card's spending requirement.

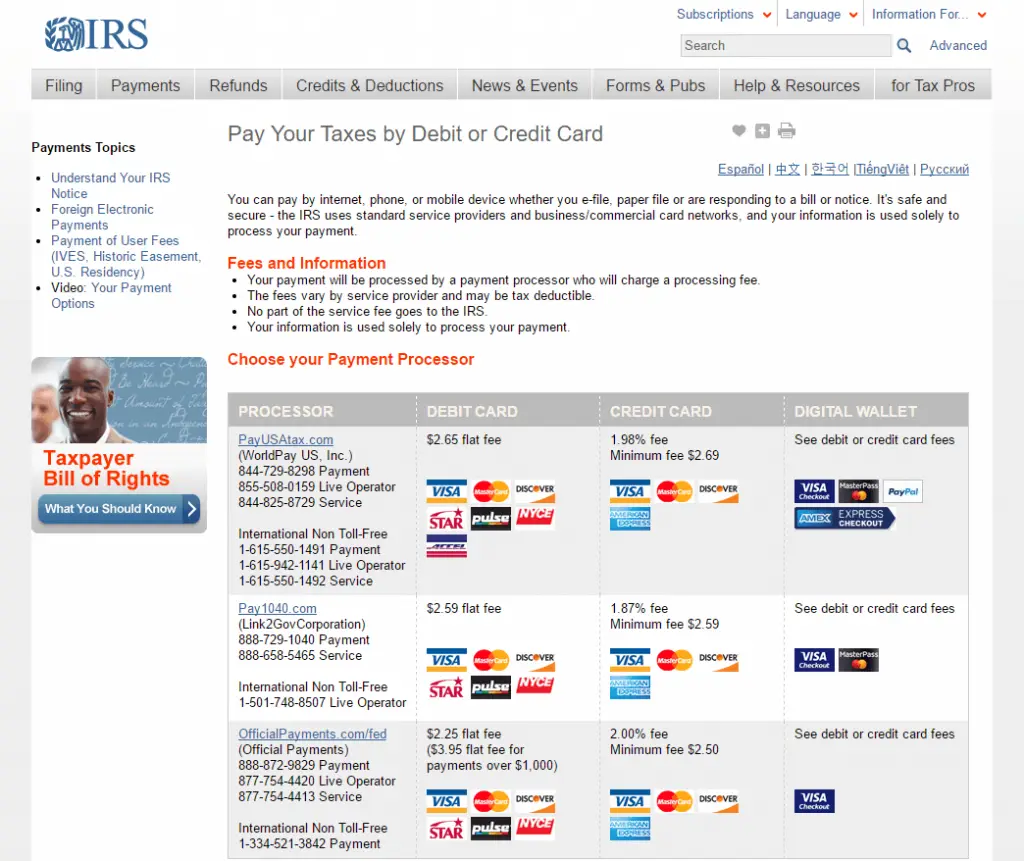

6. Use a credit card processor to pay your taxes.

If you're paying federal taxes, use one of the processors listed by the IRS that takes credit cards. If you're paying state or property taxes, check out the service Official Payments.

There is a catch: Payment processors charge fees for credit card payments — for example, Pay1040.com charges a 1.87% fee. So consider using this method only if your card has a valuable signup bonus or you don't owe much in taxes.

7. Pay your taxes in advance.

You can get a jump on your tax bill by paying taxes in advance. If you overpay, you'll get a refund from the government after you file your tax return.

8. Pay quarterly taxes.

Most people pay their taxes once a year. But did you know that most sole proprietors — such as freelancers and consultants — pay taxes quarterly? These taxpayers have regular tax bills they can leverage to hit credit card spending requirements more quickly.

Why do sole proprietors pay taxes quarterly?

Not all sole proprietors pay quarterly taxes, but many do. You're required to pay quarterly if you expect to owe $1,000 or more when you file your taxes.

Why does the government set this requirement? Because Uncle Sam wants to get paid year-round. If you're an employee, taxes are withheld from each paycheck. But that doesn't happen if you're a sole proprietor.

If you're an employee, you may be able to score this deal. First, form a sole proprietorship. Then ask your employer if they can pay you as a consultant or freelancer.

You don't have to reach your spending requirement solo. In fact, you might be surprised how easy the process can be if you enlist your friends and family.

9. Add an authorized user.

If you regularly give money to your spouse or kids, consider adding them as authorized users to your credit card account. Their spending may count toward your minimum spending requirement. As an added sweetener, you might earn points, miles or cash back from their spending.

Ask your card provider for the scoop on adding authorized users. You may have to pay fees when adding new cards, so consider whether the cost is worth the rewards you'll get. Finally, remember that you're ultimately responsible for the debt accumulated by your authorized users.

10. Add your friends as authorized users.

It's unusual to add your friends as authorized users, but you can do so if you need extra help hitting your spending requirement. Your buddies can spend on your card account and pay you back later.

11. Pay for dinner.

The next time that dinner check arrives, pay for the meal and ask your friends to pay you back. They can send you money using any one of the excellent payment apps out there, such as Venmo and Google Pay.

Google Pay is one of the best payment apps for domestic money transfers.

12. Buy things for your friends.

Ask your friends if they're looking to make large purchases. Then buy the items and have your friends pay you back.

You can also try paying for your friends' weekly expenses, such as their grocery bills. This might come with more hassle, though, as the purchases will be smaller, and you'll probably need to be there in person.

Certain expenses will come around sooner or later. Instead of waiting to spend money until you have to, spend while you're trying to collect your signup bonus.

13. Book your holiday trip.

If you plan on taking a trip this (or next) year, consider charging it to your credit card. You can score some great deals if you book early, and you can usually cancel plans if you change your mind.

Some cards will give you bonus points or miles for travel spending. For example, the Capital One Venture Rewards Credit Card offers 2x miles on all purchases.

Is there a best time to buy and save on airfare?

According to a study by CheapAir.com, it's best to buy a domestic flight 54 days out. The optimal timing varies for international flights — for example, 120 days out for Europe, 160 days for Asia and 70 days to Latin America.

14. Buy gifts in advance.

Birthdays and holidays come around like clockwork. That's a good thing, because it means you can get a jump on your gift shopping. Plus you can avoid the holiday-season retail rush.

15. Maintain your car.

If you've put off maintenance on your car, it could be a good time to get an inspection. You can also perform necessary repairs that you'd have to do later anyway.

16. Update your home.

Have you been waiting for the "right time" to renovate your home? Consider getting the job done by charging a few purchases to your card — now's a great time to change the carpets or replace old appliances.

Manufactured spending is a secret strategy in the travel-hacking community. In general, it involves buying things that you can easily liquidate to pay off your credit card.

Manufactured-spending strategies change all the time — especially when businesses and card providers make rules to circumvent them. Before using a method you see here, do some research to see if it's still valid.

17. Buy money orders with your credit card.

If your supermarket allows it, you can use your credit card to buy a money order. Afterward, deposit the money order into your bank account and pay off your credit card bill.

Most supermarkets don't allow this due to the potential for fraud — though some smaller ones will. Further, your card provider may classify money orders as cash advances, so first confirm that you won't be hit with the fees associated with them.

18. Buy and resell items.

Consider using your credit card to buy merchandise — preferably at a discount — and then resell it.

Here's a pro tip: Buy items through shopping portals like Southwest's Rapid Rewards Shopping or United's MileagePlus Shopping. This way, you can earn points on top of scooping up inventory.

Buy merchandise through Rapid Rewards Shopping and earn points for flights.

19. Open a bank account.

Some banks will let you use your credit card to make deposits into a new account. With this method, first make sure your bank allows deposits by credit card. Then make sure your card provider doesn't classify your funding as a cash advance.

20. Gift card churning.

Gift card churning involves buying gift cards and then reselling them at a break-even price — or even a loss. You can buy and sell gift cards on platforms like Gift Card Granny, Cardpool and eBay.

21. Payment-app cycling.

If you need a little boost ahead of your minimum-spend deadline, try payment-app cycling. Just use your credit card to send money through an app like Venmo — then have your recipient send the money back to you. Most card providers code Venmo transfers as purchases, not cash advances.

Credit card transfers often come with fees. (On Venmo, for example, using a credit card costs 3% of the amount sent). That said, it's best to use this strategy sparingly.

RIP: The Target REDcard hack

The Target REDcard™ Credit Card hack was an incredibly effective strategy back in the day. It involved getting a REDcard debit card, loading funds with a credit card and then using the debit card for everyday expenses. Many travel hackers turned the method into a manufactured spending strategy — they'd load their debit cards and quickly withdraw the money to their bank accounts.

Eventually, Target barred customers from loading REDcards with credit cards. When travel hackers started loading REDcards with Visa Gift Cards, Target eventually changed the rules to only allow cash loads.

Rest in peace, Target REDcard hack. It was great knowing you.

While at the end of our list, these hacks are just as good as anything else you can try.

22. Peer-to-peer lending.

To reach your minimum spending requirement, you don't have to spend money — you can lend it.

That's where peer-to-peer (P2P) lending comes in. You'll make loans to other people and be repaid with interest. It's essentially a way to park and even get a return on your extra money. Just make sure that you won't need the money for a while.

For P2P lending platforms, try Upstart, LendingClub or Prosper. If you're OK with not earning a return on your money, consider microlending platforms like Kiva.

23. Donate to charity.

Making charitable donations is a great way to get closer to your minimum spend. If you already donate every year, you now have a reason to do it earlier. And if you're not a regular giver, you can become one now. As an added benefit, most charitable gifts are tax-deductible.

24. Buy general-use gift cards.

Visa or American Express gift cards are great choices because you can use them anywhere. Just remember that they have activation fees, and only buy them if your card provider doesn't classify such purchases as cash advances.

25. Pay for business expenses.

You might use a company credit card for work-related expenses. If so, ask your employer if you can use your own credit card for those purchases and get reimbursed later.

More guides on Finder

Source: https://www.finder.com/how-to-meet-minimum-spend-for-credit-card-bonus